When last we looked at the MER, we made a comparison of two different MER values where the rate of return, amount invested and period of time were assumed to be equal. This was to illustrate how the different MERs (low MER of 0.33%; high MER of 2.18%) impact investments in the long-term. Over 10 years the money invested, the high MER consumed 12% of the entire investment amount, compared to only 1.7% by the low MER. In the words of John Bogle, founder of Vanguard Group which manages 2 trillion in assets, “the magic of compound returns is overwhelmed by the tyranny of compounding cost.”

In Canada, MERs typically range from 0.12% to 3% with the average at 2.15%- the highest in the world according to a 2013 Morningstar report. Investing strategies indicate where within the range the MER falls; higher MERs are associated with actively managed funds while lower MERs are associated with passively managed funds.

The Difference between High and Low MERs

Actively managed funds are operated with the intent to achieve better than market returns by reacting to changes in market conditions. Fund managers are employed to buy and sell holdings in the fund. Ongoing trading activities increase operating costs with each buy and sell transaction and therefore result in a higher MER.

On the other hand, passively managed funds (such as an index fund or ETF) rely on computerized algorithms generate market returns through replicating the performance of a given index. Fund managers are employed to monitor the accuracy of the fund compared to the index. There is very little trading activity involved. The limited portfolio turnover means that operating cost are kept to a minimum which results in a lower MER.

The difference investment management style ultimately begs the question: does paying higher fees give the best bang for the buck and result in higher investment returns?

A Real-Life MER Comparison

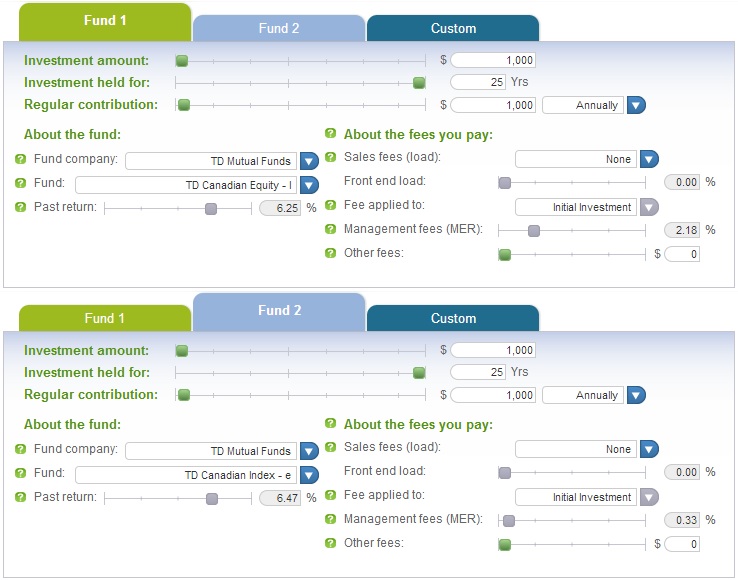

Instead of playing pretend with a hypothetical situation, a real world example works best to compare the effect of the MER between an actively managed and a passively managed fund. TD’s actively managed i-Series Canadian Equity Fund (TDB161) is focused on “high quality equity securities … judged to offer high growth potential” for investors. TD’s passively managed e-Series Canadian Index Fund (TDB900) is described to “track the performance of the S&P/TSX Composite Total Return Index.” The two funds share the same 7 of 10 top holdings (though in different distributions) and could be considered “cousins,” so to speak. Fancy that, the MER for TDB161 and TDB900 are 2.18 and 0.33%, respectively.

For the calculations, we’ll assess the fund performance using a mutual fund calculator, courtesy of the Investor’s Education Fund. The tool bases its calculations on the average return for the fund using data provided by Morningstar. The calculator estimates the past return for TDB161 and TDB900 to be 6.25% and 6.47%, respectively.

[table]

Fund, TD’s i-Series Canadian Equity Fund (TDB161), TD’s e-Series Canadian Index Fund (TDB900)

Investing Strategy, Active, Passive

MER, 2.18%, 0.33%

Past Return, 6.25%, 6.47%

[/table]

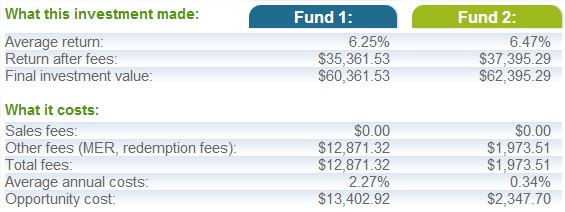

Let’s assume annual contributions of $1000 are made annually. The calculator estimates that the investment in TDB161 would grow to $60,361.53 while TDB900 would grow to $62,395.29 over a period of 25 years.

Over the same period, TDB161 would be subject to $12,871.32 in fees, resulting in a fund value of $47,490.21. TDB900 would incur $1,973.51 in fees resulting in a fund value of $60,421.78. That’s a difference of $12,931.57! As our example would have it, it just so happens that the passively managed TDB900 with the lower MER was the best bang for the buck, outperforming TDB161 over the time period considered by the IEF fund calculator. After factoring the fees the actively managed fund trailed the passively managed fund by a significant amount.

The Last Word

It’s important assess the value of the services offered through the fees associated with investing in any given fund. Understanding the fund’s MER and what it covers will help make informed investing decisions. Are you investing in TDB161 because you are confident that the TD Management team will have the ability and foresight to outperform the market through buying and selling holdings within the fund? Or are you investing in TDB900 because you believe markets will result in better returns over the long term? Neither case is particularly cut and dry as past performance isn’t an indication of future results and the MER is never an indicator of the fund’s performance. Determine the value for which you’re willing to pay to make a decision accordingly.

Have you ever encountered a fund with a higher MER that was worth the cost or a fund with a low MER that wasn’t?