Let’s take a look at the spending habits of two different families: the Flintstones and the Jetsons. The Jetsons have high-flying contraptions and a robotic maid while the Flintstones own an automobile powered through the courtesy of Fred’s two feet. For all intents and purposes let’s assume that the Jetsons have an income 10 times greater than the Flintstones. If both the Jetsons and the Flintstones spend the same $500 dollars on eating out at restaurants, who is using the money more wisely? Conversely, if a $50k single income family is able to sock away $30K into savings, that must surely be more laudable than the millionaire family that saving the same amount. Whether your income is $50k or $500k, a closer look at your budget will reflect your priorities.

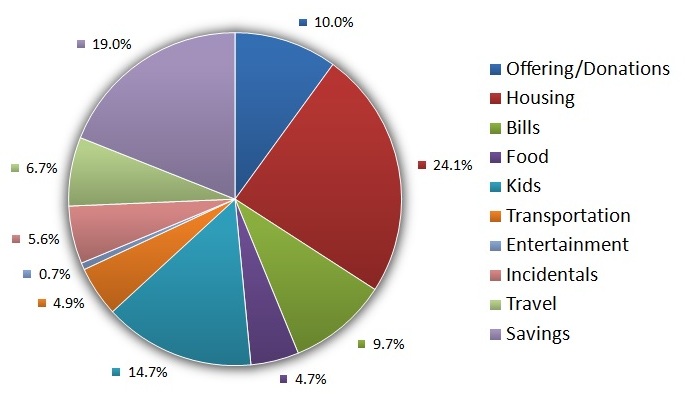

I previously touched on the process that we used to come up with our budget in the Simple Steps to Creating a Budget. We’ve charted our budget out as a percentage of our salary as we feel it has the potential to be more relatable and valuable than actual dollar values. However, the information isn’t entirely useful without a little bit more context; a percentage breakdown doesn’t describe the entire scene. Allow me to paint our budget like an impressionist. While I’m not entirely comfortable letting you rummage through my sock drawer just quite yet, I will tell you that we pull in a combined gross annual income north of $100k. That, combined with the percentages, should be enough to give you an idea of where our money goes and what we consider our spending priorities. Think of our budget like Monet’s Water Lilies – it may look somewhat fuzzy, but you get the picture.

Our monthly expenses are broken down into the following categories:

Offering/Donations

Offering/Donations

We give to our church and to several charitable organizations.

Housing

This represents the largest chunk of our monthly expenses and is made up of biweekly mortgage payments, property tax and home insurance.

Bills

The majority of this consists of our condo maintenance fees. In addition to including water and electricity, it covers the common elements and amenities including the pool, the sauna and small gym. We round this out with the internet, our home phone and cell phones. I have an unlocked iPhone4 while Emily uses a prepaid cell; we both go without data.

Food

If we eat it, it goes here. From grocery stores, farmers markets and pick-it-yourself; restaurants included.

Kid

This category can pretty much be summed up with one word: daycare. The little goat also gets a small cumulative allowance fund that covers anything from diapers and clothes to bigger one-off items such as a carseat or stroller. If we don’t use it, it rolls over to the next month. We call it a roller.

Transportation

Our trusty Corolla c. 2002 is by no means on its last legs. The monthly costs account for car insurance, gas, and a roller for projected car maintenance. Emily takes the public transportation to work.

Entertainment

Date nights, concerts, shows, family day trips and activities with the kid. Impossibru?!! Maybe we’ll let you in on our secret.

Incidentals

Part of this line item goes towards a “his and hers” allowance. This gives us the flexibility to pool our savings month over month and save up for items that are more wanted than needed: new clothes, gadgets and the like. Included are also rollers for personal care and gifts.

Travel

We’ve covered The Best Reasons to Travel and we’ve made it one of our priorities. When it comes to travelling, you really do have to see it to believe it.

Savings

At this point, we’ve fixed an amount on everything that we need to live and have also included some additional accoutrements. The remaining surplus goes into the saving vehicles of our choosing: RRSP, TFSA, RESP, and/or additional mortgage payments.

Now that you’re done admiring the artwork don’t forget to visit the guest shop on your way out.

We’ve set the values as a moving target. If we miss in a particular area, we see if that trend continues and then rebalance the budget. If we hit the target, then we’ll look to hone in on some new targets. We keep a close eye on the numbers on a regular basis and will share the successes and areas in need of improvement as we roll along.

What picture of spending habits do you paint? Where does the majority of your money go?

Definitely the majority of our spend goes to the mortgage each month. But we are plowing through that baby. It’s where all my money focus is going – to have my house paid in full.

Thanks for stopping by. The mortgage/housing cost is probably going to be the lion’s share for most families. Paying it off before its amortization period is our goal!

We have a tendency to pay down debt instead of save or invest a lot of extra money. For instance, we paid off our mortgage in five years and currently we are paying off our new SUV in 2 years instead of the typical 5-7 years. I’ll tell you, that’s a big chunk of change coming out of the account every month.

I’d be ashamed to post our eating out and grocery numbers. We’re so busy and enjoy eating out a lot so those numbers can skyrocket quickly. We also buy expensive organic food most of the time so the grocery spending is equally high. I try not to think about it and chalk it up to keeping my wife happy and my family healthy 🙂

Wow, congrats on a mortgage paid in 5 years! Paying down debt is a great tendency and one that we’re working on to generate that extra money to invest.

We used to spend quite a large amount on eating out and groceries until we realized that we could up the quality of the food we were taking in while keeping costs down. Emily is just starting to look into buying organic, so the groceries may sneak up a little down the road.